Renting a car may look simple at first. But when you reach the rental counter, you may hear many confusing terms like Collision Damage Waiver, Loss Damage Waiver, Supplemental Liability Insurance, and Personal Accident Insurance. Many travelers feel unsure about what these options mean and whether they really need them.

A Collision Damage Waiver (CDW) is a type of rental car protection offered by car rental companies to help reduce your financial responsibility if your rental vehicle is damaged, stolen, or involved in an accident.

Even though many people call it CDW insurance, it is not traditional insurance. It is actually a waiver agreement inside the rental agreement. This means the rental company insurance provider agrees not to charge you for certain types of damage if you follow the rules in the contract.

CDW usually covers damage from an accident or collision. Some companies include theft protection in their packages, which they call Loss Damage Waiver (LDW). This helps cover repair or replacement costs if the car is badly damaged.

It does not normally cover damage to other people’s property, medical costs, or personal belongings inside the car. You may need other products, such as Supplemental Liability Insurance (SLI), Personal Accident Insurance (PAI), or your own auto insurance.

CDW can also reduce how much you might owe for loss-of-use fees and towing charges that rental companies sometimes charge when a rental car accident coverage plan is not in place.

What Does Collision Damage Waiver Cover?

Collision Damage Waiver is designed to protect the rental car itself. It helps cover costs if the car is damaged in common situations, such as:

- Accident damage from a crash or collision with another vehicle or object.

- Damage not caused by a crash, like vandalism or weather damage.

- Theft or loss of the rental car when LDW includes theft protection.

- Loss of use fees, which are charges rental companies add when the car can’t be rented out while being repaired.

- Towing and administrative fees may be incurred after an accident.

This means that if something happens to the car while you are renting it, you may not have to pay the full repair bill or the rental company’s costs yourself if you have CDW.

Optional Extensions

Some rental companies sell Super Collision Damage Waiver (SCDW) or similar products, such as Excess Reduction, that can reduce or eliminate your deductible or excess. This means you may not have to pay anything out of pocket if a covered event occurs.

How CDW Works With Other Coverage

CDW focuses on rental-car damage, not liability for other drivers, injuries, or third-party liability insurance. Most personal auto insurance and credit card rental insurance can also offer similar protection, but they work differently and may require you to pay first and then claim back later.

In simple terms, CDW can protect you from big bills if the rental car gets damaged or stolen while you are driving it, as long as you follow the contract rules.

What CDW Does Not Cover

A Collision Damage Waiver (CDW) helps protect the rental vehicle from many repair or replacement costs if it is damaged or stolen. But CDW does not protect you from everything. It is important to know what it does not cover before you decide to buy it.

1. Damage to Other People’s Vehicles or Property

CDW only applies to the rental car itself. It does not pay to fix another person’s car or other property you damage in an accident. For that, you need third-party liability insurance such as Supplemental Liability Insurance (SLI).

2. Medical Costs

If you or your passengers are hurt in a crash, CDW will not cover medical expenses or hospital bills. Medical costs are usually covered by your health insurance or Personal Accident Insurance (PAI).

3. Personal Belongings

Items such as luggage, electronics, or personal effects left in the car are not covered by CDW. For lost or stolen items, you might need Personal Effects Coverage (PEC) or your own travel insurance.

4. Damage From Negligence or Illegal Driving

If you drive under the influence, race, drive recklessly, or break the rental agreement rules, the CDW can be voided, and you may have to pay all costs yourself.

5. Excluded Car Parts

Some parts of the car may not be covered unless you buy extra protection. Common exclusions include:

- Tires, Wheels, and Rims

- Windshield and Windows

- Undercarriage or Bottom Damage

- Interior Damage (upholstery, dashboard, etc.)

These often require separate rental car protection add-ons, and rental companies may charge you directly for any damage.

6. Prohibited Uses and Contract Violations

If you use the car outside the agreed-upon locations, allow an unauthorized driver to operate it, or commit other contract violations, your CDW can be canceled. Then you must pay all repair costs yourself.

How Much Does Collision Damage Waiver Cost?

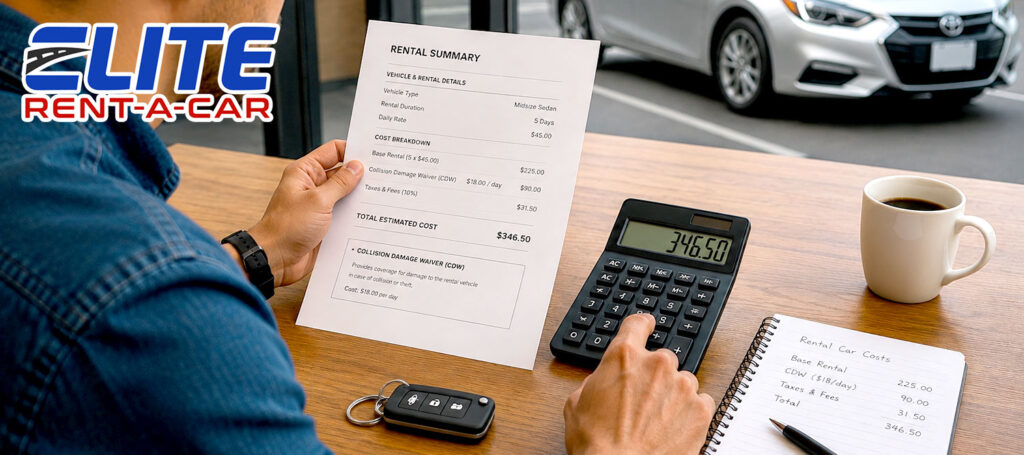

When you add a Collision Damage Waiver (CDW) to your rental car protection plan, you pay extra on top of the regular car rental price. The cost depends on the rental company, where you rent the car, and the vehicle type you choose.

Typical Daily Cost

Most rental companies charge a daily fee for CDW:

- CDW often costs about $10–$30 per day for many vehicles.

- In some cases, costs can be $20–$45 or more per day for larger or higher-value cars.

- For basic economy vehicles, many rates fall in the $15–$42 per day range.

These amounts are in addition to your regular rental car coverage and the cost of your rental agreement.

What Affects the Price

Several things can change how much CDW costs:

- Rental Location: Renting at an airport or a busy city can cost more.

- Car Type: Bigger or luxury cars usually cost more to protect.

Total Cost for a Trip

If you rent for many days, the daily CDW fees add up. Even a short trip of a few days can cost $100 or more just for the waiver, especially if you rent a bigger car or choose extra protection.

Do You Need Collision Damage Waiver?

Deciding whether you need a Collision Damage Waiver (CDW) when you rent a car depends on your personal situation.

When You Might Need CDW

1. You Don’t Have Auto Insurance

If you do not have your own auto insurance, a CDW can help protect you from paying high repair or replacement costs if the car is damaged or stolen. Without CDW or other coverage, you could pay thousands of dollars out of pocket for a crash or theft.

2. Your Auto Insurance Has Gaps

Even if you have collision and comprehensive coverage on your regular car, it may not fully cover a rental vehicle. Some policies have limits, high deductibles, or do not cover rentals abroad. In these cases, CDW can offer added peace of mind.

3. You Want to Avoid Claims on Your Insurance

Filing a claim with your own insurance after a rental car accident could raise your premiums. Choosing CDW lets the rental company handle repair costs without affecting your personal policy.

4. You Are Traveling in a Foreign Country

In some countries, your usual auto insurance may not apply at all. A CDW or Loss Damage Waiver (LDW) can help ensure you are covered for damage without surprise costs when you return home.

When CDW May Not Be Necessary

1. Your Auto Insurance Covers Rentals Well

If your personal auto insurance already includes collision and comprehensive coverage for car rental damage coverage, you may not need CDW. But you should check the details first.

2. Your Credit Card Offers Rental Protection

Some credit card rental insurance benefits can cover damage or theft when you pay for the rental with the card. This may reduce or replace the need for CDW, though you may have to pay first and file a claim later.

3. You Have Third-Party or Travel Insurance

Travel insurance or third-party coverage can sometimes offer similar protection for a lower cost. Shopping around for the right rental car protection plan before your trip can help you avoid overpaying.

Does Personal Auto Insurance Cover Rental Cars?

Personal auto insurance often covers damage to a rental vehicle, but it depends on the type of coverage you already have and the rules in your policy.

When Your Auto Insurance May Cover a Rental Car

If your personal auto policy includes collision coverage and comprehensive coverage, it may pay to repair or replace a rental car after a crash or theft. Many insurance companies extend the same protections to rental cars that apply to your own vehicle, as long as the car is used for personal, not business, purposes.

For example:

- Your collision insurance may help pay for damage to the rental car after you pay your deductible.

- Your comprehensive coverage may apply to non-collision losses, such as theft, vandalism, or hail.

- Your liability insurance may help pay for damage you cause to other people’s property or injuries in an accident.

Limitations of Personal Auto Coverage

Even though your personal auto insurance can cover a rental, there are some important limits to know:

1. Deductibles

Your own policy may require you to pay a deductible before coverage applies. With a Collision Damage Waiver, you may avoid paying a large deductible at the rental counter.

2. Loss-of-Use and Fees

Many personal insurance policies do not cover rental company charges such as loss-of-use fees, towing charges, or administrative fees, even if the rental car is damaged.

3. Geographic Limits

Your auto insurance may not cover rentals outside your home country (for example, in many cases outside the U.S. and Canada), so additional protection, such as CDW, may be needed for travel abroad.

4. Policy Exclusions

Some policies exclude certain vehicles or uses, such as luxury cars, very long rental periods, or business use, so those cases may not be covered.

When You Might Still Want CDW

Even if your personal auto insurance covers rental car damage, you might choose to buy a Collision Damage Waiver when:

- Your deductible is high, and you want to avoid paying it.

- Your policy may have limits or exclusions that apply to the rental.

- You want to skip filing a claim with your insurer and deal only with the rental company.

Does Your Credit Card Cover Rental Car Damage?

Many credit cards include rental car protection that can help cover damage to your rental vehicle, instead of buying a Collision Damage Waiver (CDW) at the rental counter. This benefit is often called credit card rental car insurance or an Auto Rental Collision Damage Waiver, and it works differently from insurance you buy from a rental company.

How Credit Card Rental Coverage Works

To use your card’s protection, you usually must:

- Pay for the entire rental with that credit card

- Be the primary renter on the contract

- Decline the rental company’s CDW/LDW at the counter

When you do this, your credit card may cover damage or theft of the rental car — and sometimes certain fees, such as loss-of-use, towing, and administrative fees, depending on the card’s terms.

Primary vs Secondary Coverage

Credit card rental car protection comes in two main forms:

Primary Coverage

- This pays for damage or theft first, without needing to file a claim with your personal auto insurance.

- You file claims with your credit card benefits administrator.

- Some premium cards (including certain Visa, Mastercard, and American Express options) offer primary rental coverage.

Secondary Coverage

- Most credit cards provide this type.

- It kicks in after your personal auto insurance pays. For example, it may reimburse your deductible and other costs your policy didn’t pay.

- Secondary coverage is common and still useful, but you usually file first with your own insurer.

What Is Super Collision Damage Waiver (SCDW)?

A Super Collision Damage Waiver (SCDW) is an enhanced form of Collision Damage Waiver (CDW) that offers more protection when you rent a car. It is an optional extra you can buy with your rental car protection plan.

What SCDW Does

- SCDW reduces or eliminates your excess (the amount you must pay if the rental vehicle is damaged). A standard CDW or Loss Damage Waiver (LDW) usually has a deductible or excess you must pay first. With SCDW, that excess can be reduced to zero.

- It often covers more parts of the car than basic CDW, including areas that may be excluded from standard coverage, like tires, windshield, undercarriage, and other components.

- Some rental companies call it Excess Reduction, Premium Protection, or Enhanced Collision Damage Waiver. These names all refer to the same idea: extra protection beyond basic CDW.

Why You Might Choose SCDW

- A lower or no deductible means you may not have to pay for damage to the rental vehicle if it occurs during your trip.

- You may avoid a large hold or security deposit on your credit card when you pick up the car. Without SCDW, companies can hold thousands of dollars as a “deposit” for excess. With it, the pre-authorized hold can be much smaller or removed.

- SCDW can help provide extra peace of mind on long trips or in areas where the risk of damage is higher.

How SCDW Works With Your Rental

- You can usually choose SCDW at the rental counter or when booking online.

- It is not mandatory, but many travelers pick it to reduce the financial risk of damage or theft.

- Even with SCDW, you must still follow the rental agreement rules to keep coverage valid.

Common CDW Mistakes Renters Make

When you choose a Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) for a rental vehicle, many people assume it will protect them from everything. This is not true, and these mistakes can lead to big bills later. A CDW is a contractual waiver, not full insurance. You must read the rental agreement carefully to know exactly what you are agreeing to.

1. Thinking CDW Covers Everything

Many renters assume CDW pays for all damage. In reality, it usually only covers damage to the rental car’s bodywork and may still require an excess or deductible. Common exclusions like tires, wheels, windshield, and glass are often not covered unless you buy extra protection.

2. Ignoring Exclusions in the Contract

Each rental company’s terms are different. If you don’t read the rental car coverage details, you may be surprised by what is excluded. For example, glass breakage or tire damage might be your responsibility even with CDW.

3. Assuming CDW Is Insurance

CDW or LDW is not traditional insurance, even though many people call it “CDW insurance.” It is a waiver that limits your responsibility only if you follow the rental rules. Violating the rules may void your coverage entirely.

4. Overlooking Loss-of-Use and Fees

Some renters think CDW covers all damage-related fees. In reality, fees like loss of use (what the company loses while the car is being repaired), towing charges, and administrative fees may not be covered unless the waiver specifically includes them.

5. Not Checking Personal Insurance and Credit Card Benefits

If you already have personal auto insurance or credit card rental insurance, you might not need CDW. Many credit cards provide coverage if you use the card to pay for the rental. But renters often skip checking these benefits and end up buying CDW unnecessarily.

6. Failing to Report Damage Immediately

If the rental car gets damaged, you usually must report it right away. Waiting or failing to properly document the damage can jeopardize your claim and leave you responsible for the full repair costs.

7. Letting Unauthorized Drivers Use the Car

If someone not listed in the rental agreement drives the car and it gets damaged, the CDW can be voided. Always add extra drivers to the contract before anyone else drives.

8. Driving in Restricted Conditions

Driving off-road, under the influence, or outside approved areas often cancels CDW protection. Rental companies may then charge you for all damage.

Frequently Asked Questions

1. Is CDW the Same as Insurance?

No. A CDW or Loss Damage Waiver (LDW) is not traditional insurance. It is a contract with the rental company that waives their right to charge you for damage or theft of the rental vehicle if you follow the rules.

2. Do I Have to Buy CDW to Rent a Car?

No. You can rent a car without buying CDW. But if you decline it, you are responsible for damage or theft of the car unless you have other coverage from your personal auto insurance or credit card rental insurance.

3. What Does CDW Usually Cover?

CDW typically covers damage to the rental car from collisions, accidents, vandalism, or sometimes theft, depending on the rental company’s terms.

4. What Does CDW Not Cover?

CDW does not cover damage you cause to other vehicles or property (that’s liability), medical bills, or personal belongings. You still need liability protection and possibly other products for those.

5. Will I Still Owe Money After a Damage Claim?

Sometimes yes. Standard CDW may still include a deductible (called excess), meaning you pay part of the repair cost before the waiver applies. The amount varies by rental company and car type.

6. How Much Does CDW Usually Cost?

CDW typically costs a daily fee that depends on the rental company, location, and vehicle type. In the U.S., it often falls within a range of $10 to $42 per day.

7. Does CDW Cover Theft?

Some CDW products include theft protection, but not all of them. If your rental company only offers a basic CDW, theft might not be covered unless the contract says otherwise.

8. Can I Use My Credit Card Instead of CDW?

Yes. Many credit cards offer rental car insurance benefits that can replace CDW if you pay for the rental with the card and follow the card’s rules. This can save money, but you should check your card’s coverage details first.

9. Does CDW Help With Loss-of-Use Fees?

Yes. A CDW often waives loss-of-use fees that the rental company might charge while the car is being repaired.

10. Does CDW Cover Weather and Vandalism Damage?

It often does, but the exact coverage depends on the rental provider’s contract. Always check the fine print before you agree.